Newrez LLC services residential mortgages under its own name and, for a large part of its book, as Shellpoint Mortgage Servicing — by Shellpoint's own account it collects principal, interest and escrow for well over a million homeowners. The borrower-facing app sits on a servicing file that already carries the structured pieces an integrator wants: the outstanding principal balance, the current rate and maturity, the most recent escrow analysis, payment history, scheduled and pending payments, the year-end Form 1098, and the funding-to-active loan status. None of that has to be re-keyed. It has to be reached, under the borrower's authorization, and turned into something a system can call.

That is the job this brief scopes. Below: what the file actually contains, the route we would take to it for a US mortgage servicer, the runnable artefacts we hand over, and the specific things a Newrez build has to account for.

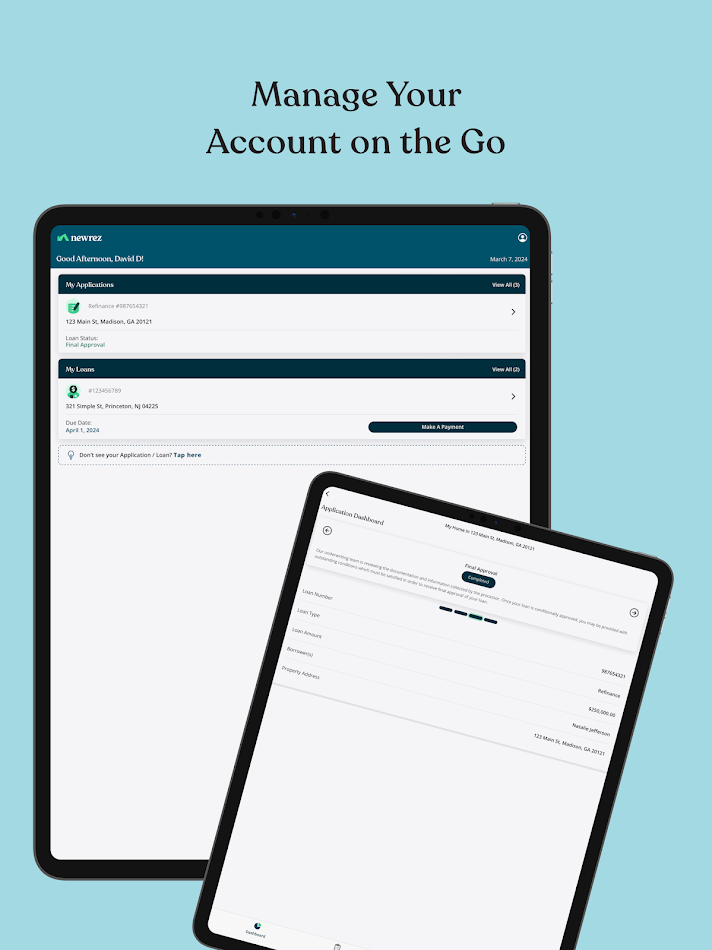

What the servicing file actually holds

Each row below is a surface a Newrez or Shellpoint borrower can see today after signing in. The grain matters more than the label: most of it is per-loan and current, two of the most-requested pieces are documents rather than fields.

| Data domain | Where it surfaces in the app | Granularity | What an integrator does with it |

|---|---|---|---|

| Loan snapshot | "My Loans" → Account Details dashboard | Per-loan, current: principal balance, interest rate, maturity, recent activity | Sync the live mortgage balance into a net-worth or PFM view; feed an underwriting model the borrower's current standing |

| Escrow | Account Details → Escrow → Escrow Analysis | Per-loan: latest analysis plus the escrow breakdown | Reconcile tax and insurance disbursements; project the payment change an analysis triggers |

| Payments | Payments section: one-time, pending, scheduled, Edit Autopay | Per-transaction and per-schedule | Build a payment timeline; flag a missed or late draft; mirror AutoPay state |

| Statements | Documents | Monthly PDF, per statement period | Archive for the borrower; parse line items into a ledger |

| Tax documents | Account Details → Form 1098 Mortgage Interest Statement | Annual PDF, available when issued | Feed mortgage interest into tax-prep or bookkeeping without manual entry |

| Loan status | Loan number → Loan Status page | State plus updates, application through funding | Track an origination pipeline; trigger downstream steps on a status change |

Reaching the loan file under the borrower's authorization

For a US mortgage servicer there are really three routes, and they are not equal here.

Interface integration on the authenticated portal

The sign-in path runs through Newrez's own auth host, which issues a session after the borrower authenticates and, where the account requires it, a step-up challenge. Working under the borrower's consent, we analyse that traffic, document the token and session chain, and build the calls that return the loan snapshot, escrow analysis, payments and status. This is the route with the most reach — it gets at everything in the table — and the one we would recommend as the backbone of a Newrez integration. Effort is moderate; durability depends on the portal front end staying stable, which is why we keep watching it for changes after delivery.

User-consented credential access

For products that already hold the borrower's relationship — a PFM, a tax tool, a lender — the same interface integration runs with the user supplying and consenting to the use of their own Newrez credentials through the integrating product. Reach is the same as the portal route; the difference is whose flow the borrower authenticates in. We set up the consent capture and the credential handling as part of the build.

Native document export

Statements and the 1098 are downloadable PDFs. On their own they are a narrow surface — no live balance, no escrow projection — but as a fallback or an archival feed they are reliable and low-maintenance, so we wire them in alongside the portal route rather than instead of it.

Access, onboarding and the consent records are arranged with the client during the engagement. For almost every Newrez use case we would build the authenticated-portal route first and attach document export for the tax and statement pieces — that pairing covers the whole file and degrades gracefully if a front end shifts.

What lands at the end of the build

Everything is specific to the Newrez surfaces above, not a generic kit:

- An OpenAPI specification covering the loan snapshot, escrow analysis, payments, statements list, 1098 retrieval and loan status as clean endpoints.

- A protocol and auth-flow report: how the Newrez sign-in host issues and refreshes the session, how a step-up challenge is carried, and how the Newrez and Shellpoint front ends differ.

- Runnable source for those endpoints in Python and Node.js, including the document-to-fields parsing layer for the 1098 and escrow analysis.

- Automated tests against a consenting account, including the session-expiry and re-auth paths.

- Interface documentation, plus data-retention and consent-logging guidance written for a mortgage servicing data set.

A statement-and-escrow pull, sketched

Illustrative only — field and path names are pinned during the build against a consenting account, not asserted here as the live contract.

# Authorize once under the borrower's consent, then read the file.

session = newrez.auth(username, secret) # -> bearer + session cookie

if session.challenge == "step_up": # MFA / OTP path

session = newrez.complete_step_up(session, otp)

loans = GET /servicing/loans Authorization: Bearer <tok>

# [{ loanId, brand: "newrez" | "shellpoint", principalBalance,

# interestRate, maturityDate, nextDraftDate }]

for ln in loans:

escrow = GET /servicing/loans/{ln.loanId}/escrow/analysis

# { analysisDate, cushion, projectedPayment, disbursements[] }

pays = GET /servicing/loans/{ln.loanId}/payments?status=all

# [{ postedDate, amount, type, status }]

docs = GET /servicing/loans/{ln.loanId}/documents?type=1098

pdf = GET docs[0].href # PDF -> parse to fields

# Error handling that actually matters here:

# 401 / session_expired -> re-auth, replay idempotent reads

# 409 challenge_required -> re-run step-up, do not loop blindly

# brand flips newrez/shellpoint -> key on loanId, not the brand

The escrow and 1098 calls return documents in practice; the parsing layer turns them into the fields shown so a caller never has to open a PDF.

Where integrators put a Newrez feed

- A personal-finance or net-worth app that wants a member's real mortgage balance and next payment, refreshed, instead of a manual entry that goes stale.

- A tax or bookkeeping tool that pulls the annual 1098 mortgage interest for self-employed or itemising filers the moment it is issued.

- A lender or broker verifying an applicant's existing mortgage standing and escrow position during a refinance or second-lien decision.

- A property or portfolio tool tracking escrow-analysis changes across several loans so an owner sees a payment change coming.

Mortgage servicing data and the 1033 question

This comes up on every US servicer build, so it is worth being exact. A mortgage servicer like Newrez is not among the financial products the CFPB's Personal Financial Data Rights rule, under Section 1033 of Dodd-Frank, currently reaches — the rule's initial scope leaves out Regulation Z creditors such as mortgage lenders. The rule itself is back in rulemaking after the CFPB's 2025 reconsideration, so its eventual shape for servicers is unsettled and this brief does not state future obligations as if they were in force. The practical consequence is simple: there is no standing open-banking consent channel pointed at a Newrez loan file. The authorized route is the borrower's own access, exercised with their consent. We operate that way as a matter of course — access logged, the data set minimized to what the use case needs, and an NDA in place where the client requires one.

Things we plan around on a Newrez build

Two specifics shape how we design a Newrez integration, and we handle both rather than hand them back as conditions.

The dba split. Newrez LLC also operates as Shellpoint Mortgage Servicing, and a borrower's loan can be presented under either brand depending on who services it — Shellpoint is Newrez's third-party servicing brand. We map both front ends and key the normalized record on the loan identifier, so a loan that is presented under Newrez today and Shellpoint later stays a single record, not two.

The platform move. Rithm Capital, Newrez's parent, has reportedly said it will roll Newrez servicing onto Valon's ValonOS platform by 2027. We isolate the authentication and document endpoints behind a thin adapter so that a platform cutover is a contained re-map rather than a rebuild. We also keep a lightweight check that compares the live portal against the documented shape and reruns on a schedule, so a front-end change is caught before a caller sees it.

A third, smaller one: the 1098 and escrow analysis are documents, not fields, so the parsing layer is scoped into the build from the start rather than bolted on.

Working with us on this

A working Newrez integration is priced from $300 for source-code delivery — the runnable endpoints, the spec, the auth-flow report and the tests — billed only after we hand it over and you have run it against your own consenting account. If you would rather not host anything, the same coverage is available as our pay-per-call hosted API: you call the endpoints and pay per call, with nothing up front. The initial build runs in one to two weeks. Tell us the app — Newrez — and what you need out of the loan file, and we will scope it; the access, onboarding and consent records are arranged with you as part of the work. Start the conversation at /contact.html.

Screens from the app

The borrower-facing surfaces, from the app's store listing — open any one full size.

Where these notes come from

Checked in May 2026 against the app's own description and the borrower-account material Newrez publishes, plus the current US data-rights position. Primary references: Newrez's step-by-step guide to online accounts and its online-portal loan-tracking walkthrough for the surfaces; the CFPB's Personal Financial Data Rights page and the Federal Register reconsideration notice for the regulatory status.

- Newrez — a step-by-step guide to online accounts

- Newrez — using the online portal to track loan approval

- CFPB — Personal Financial Data Rights (Section 1033)

- Federal Register — Personal Financial Data Rights Reconsideration

OpenBanking Studio integration desk · mapping reviewed May 2026.

Other servicer apps in the same picture

Same category, useful when the goal is one unified mortgage feed rather than one app:

- Mr. Cooper — large servicer app with balance, payments, AutoPay, statements and home-value tracking behind a borrower login.

- Rocket Mortgage — origination and servicing in one app, with payment management and document access for active loans.

- PennyMac — servicer portal exposing loan details, payments and year-end tax documents to the borrower.

- loanDepot — origination and servicing app with statements, payment history and loan status.

- Lakeview Loan Servicing — a major US servicer whose portal carries payments, escrow and documents.

- Freedom Mortgage — servicer app with payment options, statements and assistance workflows.

- Carrington Mortgage Services — borrower self-service for payments, documents and account status.

- Shellpoint Mortgage Servicing — Newrez's own third-party servicing brand, with the same class of loan, payment and document surfaces under separate branding.

- Mutual of Omaha Mortgage — origination-led servicer with an account portal covering loan and payment data.

Questions integrators ask about Newrez

Can you separate a loan that appears under both Newrez and Shellpoint Mortgage Servicing?

Yes. Newrez LLC operates as Shellpoint Mortgage Servicing for part of its servicing book, so the same borrower can see a loan branded either way depending on who services it. We map both front ends and key on the loan identifier, so the loan lands on one normalized record even if the branding it is presented under changes.

Is the 1098 and the escrow analysis available as data, or only as a document inside the app?

In the borrower portal the Form 1098 Mortgage Interest Statement and the escrow analysis are document surfaces — PDFs you view or print from Account Details. We add a parsing layer on top of the document pull so downstream systems receive structured fields (interest paid, escrow disbursements, projected payment change) rather than a file to open by hand.

Newrez sits outside the CFPB open-banking rule, so what is the authorized route to the loan file?

The route is the borrower's own access. A mortgage servicer like Newrez is not among the products the CFPB's Personal Financial Data Rights rule currently covers, and that rule is back in rulemaking, so there is no standing consent channel to point at. We operate the interface integration under the account holder's authorization, with access logged and the data set minimized to what the use case needs.

If Newrez moves its servicing onto Valon's platform, does the integration have to be rebuilt?

It does not have to be rebuilt from scratch. Rithm Capital has reportedly said it will roll Newrez servicing onto Valon's ValonOS by 2027, so we isolate the authentication and document endpoints behind a thin adapter; a platform cutover becomes a contained re-map rather than a new project, and a scheduled check that compares the live portal against the documented shape catches a front-end change before a caller does. The initial build cycle is one to two weeks.

App profile — Newrez

Newrez is the borrower-facing mortgage app of Newrez LLC, a US residential mortgage originator and servicer founded in 2008 and headquartered in Fort Washington, Pennsylvania, and a member of the Rithm Capital family of companies. The company also operates a third-party servicing brand, Shellpoint Mortgage Servicing. The app lets a borrower view a snapshot of the current loan (account details, balance, recent activity, payment info), make a one-time payment or schedule recurring payments, download statements and other documents including the Form 1098, and check loan status from application through funding. Listed on Google Play as com.newRez and on the App Store, with the company stating it is licensed in all 50 states (NMLS #3013, per its own licensing disclosure). Referenced here only to scope an interoperability integration.